Most clients have the same concerns when we first meet them.

1. They think they should be further ahead financially, and so

2. They want to know what options are available to them, because

3. They think they should be further ahead!

At some point in our lives, we all compare our worst with other people’s best and it makes us doubt ourselves. Money, health, marriage, career, kids, whatever.

It’s the way we’re wired.

And I suspect that’s what happened to a journalist I mentioned in last week’s Moowsletter.

About a month ago, a finance journalist said she was going to minimise her mortgage repayments so she could buy other assets to help fund her living standards in retirement.

The problem was, she admitted she wouldn’t have her mortgage paid off before she retired.

So why do it?

Pressure.

She’s trying to play catch-up and consequently, has chosen the wrong option…in my opinion.

Here’s why.

The best debt management strategy is to get rid of your non-deductible debt (mortgage, personal loans) as soon as possible. Period.

However, that doesn’t mean you can’t have your cake and eat it too. You can.

Meaning, you can still pay down your mortgage and simultaneously build an asset base.

Unfortunately, this lady turned her situation into a game of ‘either or’ (mortgage vs investments) when she didn’t need to.

Let me show you what I mean.

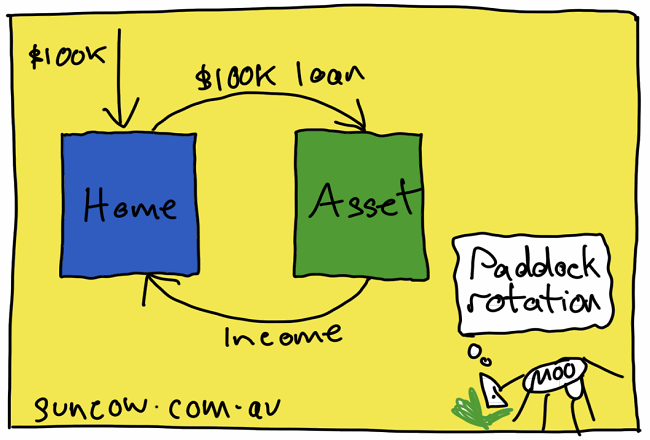

Let’s suppose you’ve accumulated $100,000 in extra repayments, or you receive a work bonus, an inheritance, sell an asset…or you’ve cleaned out the crap in your shed and you put on a massive garage sale.

The first thing you should do is drop the extra cash on your mortgage and reduce your non-deductible debt.

That one’s non-negotiable!

Then, if you want to purchase an asset, you simply redraw that money out of your home in the form of a line of credit.

Best of all, the line of credit will be tax deductible provided you use it to purchase an income producing asset.

This strategy is called ‘debt recycling’ and it works extremely well for the right client.

Here’s why.

If you borrow at, say 3%, and you buy an asset with and income yield of 5%, the investment is immediately cashflow positive.

Meaning, the income from the asset is greater than the loan repayments.

You can then use that surplus income to help pay down your mortgage faster while simultaneously building an asset base in addition to your home and super.

Make sense?

i.e. you don’t have to choose between your mortgage or buying an investment. You can do both.

Specifically, debt recycling offers 6 key benefits. You can…

1. Reduce your non-deductible debt (mortgage)

2. Buy another asset in addition to your home

3. Generate investment income to help pay down your mortgage sooner

4. Get the capital growth from both assets (long term)

5. Claim a tax deduction from the second loan (line of credit)

6. Collect a tax rebate (tax credits)

Please note – this is not a get rich strategy. It’s a cashflow strategy first, wealth accumulation second.

But you must be willing to wait.

A few weeks ago, said journalist suggested now is the time to load up on debt and buy more assets just because interest rates are low.

I couldn’t disagree more.

This market is frothier than a poorly poured beer. So just wait.

In the meantime, if you’d like to have a chat about what options are available to you, drop me a line and we can organise a ‘cake and eat it’ session.

Have a great weekend!

Adam

Warning: This Moowsletter may not be for you. If you get a little starry-eyed every time you glance at that gold band wrapped around your finger…look away now. I’m about to wipe the lust out of your peepers. (No hard feelings.) Here’s the unpolished truth about gold… If you bought $1 worth of gold 100 years …

Retirement should be a time to enjoy life, not stress over finances. A well-thought-out retirement plan ensures you can live comfortably, pursue your passions, and handle unexpected expenses without worry. The earlier you start planning, the smoother the journey will be. Let’s break it down into simple, actionable steps to help you create a retirement …

Continue reading “How to Plan for Retirement: Your Roadmap to Financial Freedom”

It’s Tuesday lunch, and all morning the markets have been drowning in a sea of red thanks to Trump’s tariffs. Investors are freaking out. But as my RM’s hit the pavement for my midday walk, I get this deep, unshakeable, hunch… “What if?” This is why my tummy turned… A month ago when Trump first …

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.