Imagine having 100 cows to fund your retirement.

This means you have two ways of generating an income. You can (a) sell the milk they produce or (b) just sell a few cows each year.

The problem with option (b) is the price of cows fluctuate and you risk selling all your cows before you die (run out of money).

My mission is simple…to help grow your money (herd) so you know how much income (milk) you’ll have each year for the rest of your life.

To help give you a better idea of how the cows stratgey works, let me share a very simple analogy I call…

They could retire with certainty. Also, their money would most likely outlive them which means they could pass it on to the kids, if they wanted to.

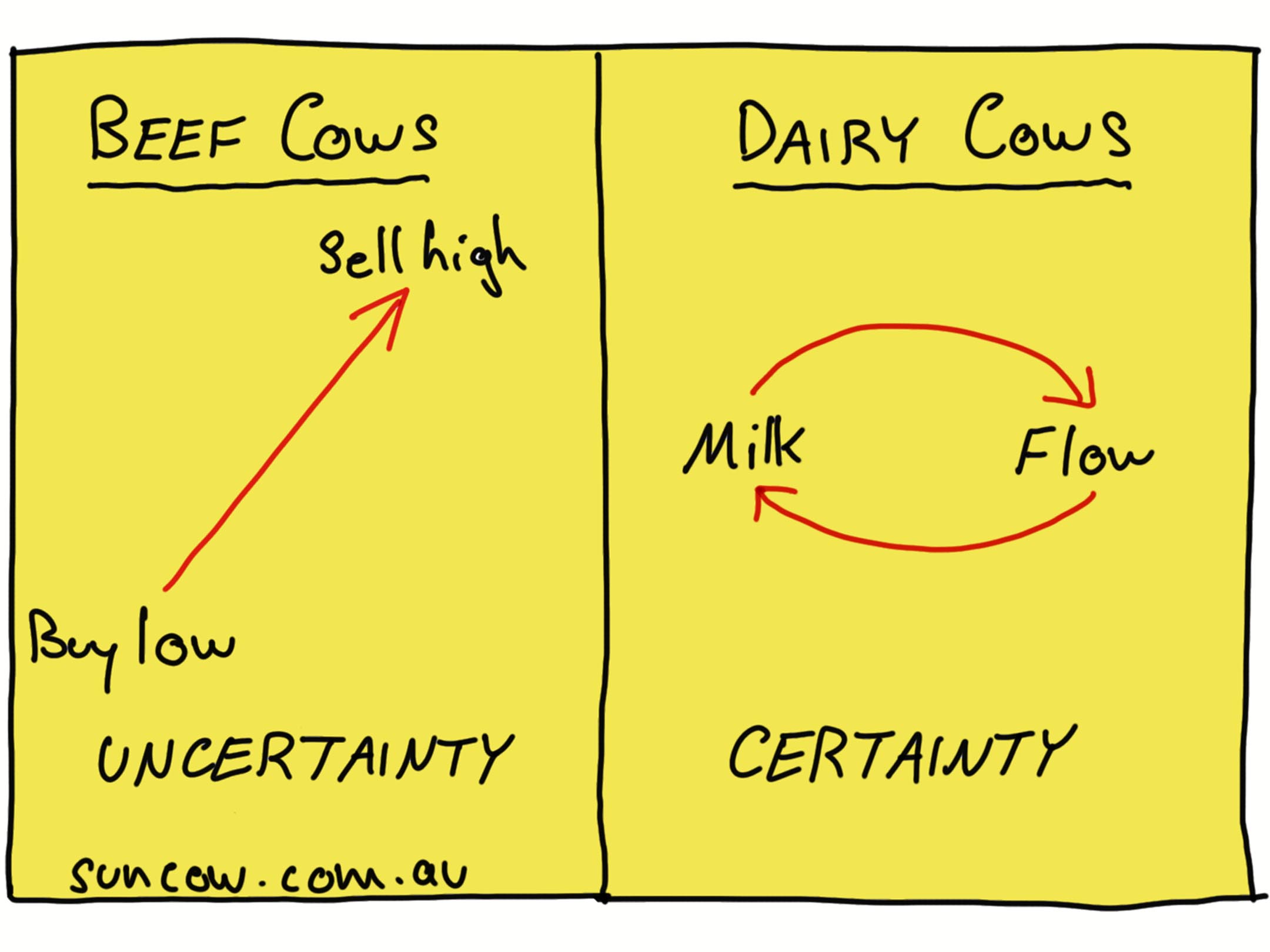

They could retire with certainty. Also, their money would most likely outlive them which means they could pass it on to the kids, if they wanted to. Beef Cattle: suppose you’re a beef farmer. Your model for making money is to buy young calves at a low price (say $200 each) and grow them into much bigger cattle to sell at a higher price (say $1,000 each). The difference is the profit which becomes your income.

But the problem with being a beef producer is you’re always up against the vagaries of the markets and the weather (e.g. floods, drought), all of which you have no control over. Therefore, your method of generating an income is riddled with uncertainty.

Unfortunately, this is exactly how most people invest. They invest like beef farmers. They hope to buy low and sell high and rely on the profits to create wealth, especially in retirement.

So, what’s the alternative?

Dairy Cattle: now, suppose you’re a dairy farmer instead (lucky you!). Your model for making money is to maintain a herd of dairy cows that get milked twice a day, 365 days a year. Their constant milk flow becomes your constant cashflow.

Simply put, when you wake up on January 1 every year, you know within close proximity how much milk your cows will produce and therefore what your income will be for the year.

This is the investment approach we subscribe to at Suncow. We recommend clients build an asset base that generates good consistent cashflow, regardless of the markets because it delivers greater certainty.

But wait, it gets better…

Let’s imagine for a moment, your super is just a tax effective paddock and the only difference is the type of cows you put in your paddock.

This is where investing like a dairy farmer inside super is very powerful.

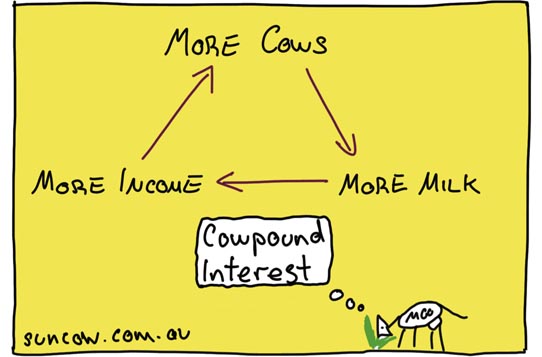

Suppose you have a herd of dairy cows in your super and all you do is sell the milk to buy more dairy cows. Your herd gets bigger which means it produces more milk enabling you to buy even more cows.

And then it grows again which means more milk, more cows, more income…

At Suncow, we call that ‘cowpound interest’. It’s the best way to grow your money.

And that’s all you need to do with your super. Just keep growing your herd until it’s time to retire and then live off the income.

And don’t worry about how much your herd (portfolio) is worth, just concentrate on how much milk (income) it produces.

If you focus on compounding the growth of your herd by reinvesting, you will never have to rely on the markets to grow your super. Nor will you be affected when the markets go down either.

Make sense?

Investors are attracted to beef cattle because they love to watch their investments appreciate in value. It makes them feel wealthy and they think it’s the only way to make money. E.g. when an investment goes from $10 to $20.

However, the irony is this…

It’s the difference between the goose and the golden egg.

The beef farmer just wants to breed a big fat goose that he can sell (and then start over again). The dairy farmer prefers to look after the goose and live off the golden eggs.

Beef farmers buy and sell, dairy farmers buy and hold.

Get my drift?

“Yeah but…” I hear you say.

Good question.

Imagine you see a cow standing in a paddock happily grazing, making milk. And the next day, the market for cows falls through the floor. Do you think she’s going to eat less and produce less milk just because she’s worth less? Of course not.

If the market drops, she’ll still eat the same amount of grass and produce the same amount of milk regardless of how much

she’s worth. The money still flows in for the farmer.

It’s the same with the stock market. If the market crashes, do you think people will stop buying groceries, disconnect their gas and power, close all their bank accounts and cancel their phone accounts. Of course they won’t.

The tail doesn’t wag the dog.

The only way to plan for retirement is to build an asset base that spins off plenty of cash without relying on the markets going up.

That’s why investors freak out when the markets drop. They’ve got the wrong strategy in place.

They’re investing like beef farmers instead of dairy farmers.

So, by now you’re probably wondering…how much do I need to retire?

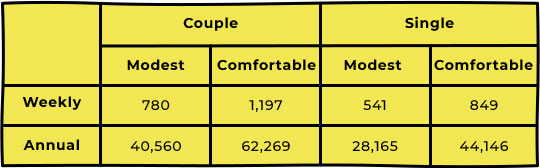

Source: Association of Super Funds Australia (ASFA) Retirement Standard Benchmarks

The Difference Between Modest and Comfortable

A modest retirement lifestyle is considered better than the Age Pension, but still only allows for the basics. I.e. no health insurance, a three-blanket heater in winter and scaring yourself to death every time you book the car in for a service.

A comfortable retirement lifestyle enables an older, healthy retiree to be involved in a broad range of leisure activities, being able to turn the air-con on in summer, top health cover, a reasonable car, good clothes, and one domestic holiday each year.

This all sounds great but where do I start and how do I know I’m doing the right thing?

I understand, I hear that all the time.

And that’s why I recommend you begin with our One Page Financial Plan.

It’s a low-risk, low-cost way of getting started.

Most importantly, we’ll address your two most important questions…

How much do you need for to retire and will you have enough?

The cost is a flat fee of $550 (inc gst) plus ninety minutes of your time.

Email me at adam@suncow.com.au to book your ninety-minute discovery meeting.

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.