George is confused and he doesn’t know who’s advice to take.

A few weeks ago he received a juicy commission cheque and his accountant suggested he stick it in super before June 30 to save some tax.

But…if he was happy to stomach some extra risk he should buy an investment property and negatively gear it.

Meanwhile his poor wife is sitting bolt-upright in bed worried about their mortgage. It’s due for refinancing and she’s begging him to wait and see what the repayments will be.

What should he do?

In an ideal world he should do both. Stick as much as possible into super to save some tax and then slap the rest on the mortgage.

But on this occasion I agree with his wife. Sacrifice the tax saving and wait.

This scenario is very common. Clients often ask if it’s best to put any surplus cash on the mortgage or invest it?

Here’s the process I took George and his wife through to better understand my thesis…

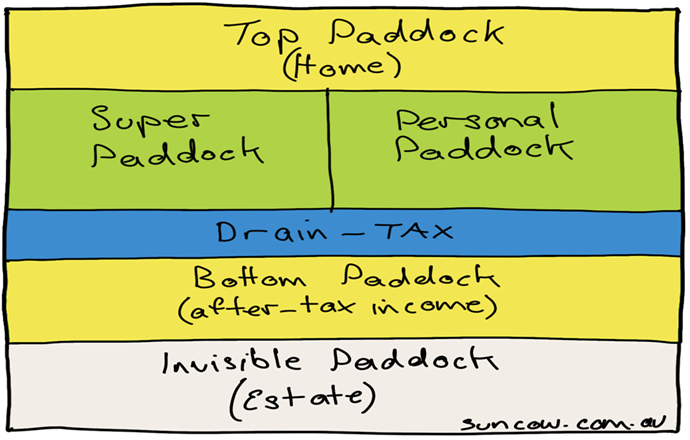

At Suncow, we split our clients finances up into five paddocks.

However, for the sake of this Moowsletter I’m going to focus on the top three paddocks only…

The top paddock is your principle place of residence. This paddock is tax free which is great when you sell your home however the loan is non-deductible.

Underneath the top paddock are your two wealth building paddocks – super and non-super (or personal).

Both these paddocks are taxable which means any income or capital gains are taxed. However any loans used to buy those assets are also deductible.

Therefore, the ultimate goal is to maximise the amount of money you get across the drain (tax) into your bottom paddock (after-tax dollars) for retirement.

Now back to George and his wife…

As a general rule, I recommend clients prioritise their paddocks in this order – top paddock, super paddock, and then personal paddock.

In other words, get your house paid off first because the debt is non-deductible.

For most people, not only is their mortgage their biggest expense but it’s their most expensive because they have to pay it off with after-tax dollars. i.e. no tax relief

Once the house is paid off, your next priority should be to jam as much money into super because the maximum tax rate is 15% and 0% in retirement.

Super is just a tax-effective paddock and it’s still the best game in town.

Finally, any surplus cash should be used to buy assets in your personal or non-super paddock.

The downside to building wealth in your personal paddock is it’s taxed at whatever your marginal rate of tax is. The upside is any debt is deductible.

Put simply, the best option for most people is to get rid of their non-deductible debt first – mortgage, personal loans, cards, etc.

The solution for George was simple.

Listen to your wife!

Have a great weekend!

Adam

Back paddock – collectively, the world spends 720 billion minutes a day using social media platforms. Over a full year, that adds up to 500 million years – GWI consumer trends report.

Warning: This Moowsletter may not be for you. If you get a little starry-eyed every time you glance at that gold band wrapped around your finger…look away now. I’m about to wipe the lust out of your peepers. (No hard feelings.) Here’s the unpolished truth about gold… If you bought $1 worth of gold 100 years …

Retirement should be a time to enjoy life, not stress over finances. A well-thought-out retirement plan ensures you can live comfortably, pursue your passions, and handle unexpected expenses without worry. The earlier you start planning, the smoother the journey will be. Let’s break it down into simple, actionable steps to help you create a retirement …

Continue reading “How to Plan for Retirement: Your Roadmap to Financial Freedom”

It’s Tuesday lunch, and all morning the markets have been drowning in a sea of red thanks to Trump’s tariffs. Investors are freaking out. But as my RM’s hit the pavement for my midday walk, I get this deep, unshakeable, hunch… “What if?” This is why my tummy turned… A month ago when Trump first …

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.