On Tuesday morning, a prospective new client asked me bluntly…

“What’s your biggest weakness?”

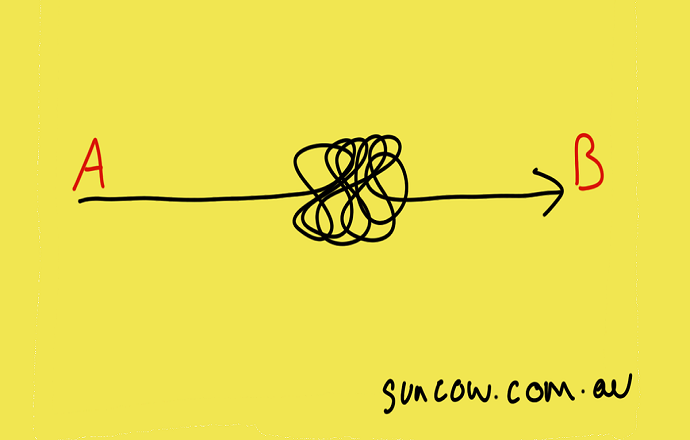

It’s a hell of a good question and one I’ve ruminated plenty of times while doing the bay run, especially the past year.

This was my blunt answer…

“I sell straight lines”

“Meaning, if you do A,B,C you’ll achieve X,Y,Z.”

And going by the look on her face, that’s not what she wanted to hear.

“But that’s why I came to see you!” she said a tad disappointed.

So I pressed on…

“The real reason you came to see me is you want to know if you can afford to turn the air-con on when you retire, spoil the grandkids with a sneaky trip to the shops, and then hop on a plane and disappear at will!”

“Correct?”

“YES! How did you know?” she said with relief.

In principle, straight lines are a great idea because they give us clarity and with clarity comes a feeling of certainty and peace of mind.

Straight lines also mean progress, the ultimate source of happiness.

But the reality is our wheels will wobble at some point.

Meaning, there will always be a messy middle – divorce, death, illness, relocation, markets going the wrong way, or some other whatnot.

The messy middle can also be very painful. Straight line clarity is replaced with hairpin bends and a loss of expectation, even if only temporarily.

Last weekend, I wrote a Moowsletter titled, Recession Proof Investments.

I then followed up with a video to our clients suggesting we’ll get a stock market correction of 40-50%.

Heavy stuff hey!

Prima facie, this would be very unsettling for most.

But here’s the thing. If you know every straight line will eventually bend, then the ultimate measure of success should be how well you manage the bend, the messy middle.

The purpose of last weeks Moowsletter was to educate readers about what to focus on when things get tight economically. i.e. investment income instead of capital gain.

To help you understand my point, consider this juxtaposition…

Most people know how much they earn from their paid work but have no idea what their employer’s business is worth. It’s irrelevant.

Yet, most people know how much their super is worth but have no idea how much income it generates.

See the paradox?

We go to work to earn an income so we should build an asset base focused on income as well.

It’s the best and surest way to manage the messy middle, especially when planning our retirement.

Focusing on the value of your super (or any other asset), is as non-sensical as focusing on the value of your employer’s business. It’s meaningless.

Income doesn’t rely on the markets going up nor is it affected when the markets go down. It’s a myth.

It’s analogous with saying the gas pipe and the water pipe going into your house are the same thing. They’re totally unrelated.

In my opinion, income should be your first reason for investing and capital gain should be your second.

Investment income is much more predictable and resilient than capital gain. It’s the best way to manage the messy middle before it happens.

Capital gain feeds your ego, income feeds your belly.

To put it bluntly.

Have a great weekend!

Adam

Back paddock – don’t try and find the needle, buy the haystack instead – Jack Bogle

Warning: This Moowsletter may not be for you. If you get a little starry-eyed every time you glance at that gold band wrapped around your finger…look away now. I’m about to wipe the lust out of your peepers. (No hard feelings.) Here’s the unpolished truth about gold… If you bought $1 worth of gold 100 years …

Retirement should be a time to enjoy life, not stress over finances. A well-thought-out retirement plan ensures you can live comfortably, pursue your passions, and handle unexpected expenses without worry. The earlier you start planning, the smoother the journey will be. Let’s break it down into simple, actionable steps to help you create a retirement …

Continue reading “How to Plan for Retirement: Your Roadmap to Financial Freedom”

It’s Tuesday lunch, and all morning the markets have been drowning in a sea of red thanks to Trump’s tariffs. Investors are freaking out. But as my RM’s hit the pavement for my midday walk, I get this deep, unshakeable, hunch… “What if?” This is why my tummy turned… A month ago when Trump first …

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.