How the tables turn.

Twelve months ago, most people had no idea what franking credits were.

Today, they’re being discussed in every bar and barber shop. Especially when voters, mostly retirees, know they will take a direct hit to the hip pocket of between $5,000 -$8,000 pa (average) if Bill Shorten wins the election on May 18.

But if Labors Retirement Tax isn’t enough, it’s the blatant lies and deceit that are being peddled by Bill Shorten and Chris Bowen that I find just as galling.

Chris Bowen made so many mistakes in his first week of the election campaign the Labor machine had to bench him until further notice.

The purpose of this Moowsletter is to clear up a few facts specific to franking credits that Mr Shorten and Mr Bowen so brazenly obfuscate without batting an eyelid.

But before I do, here’s a quick recap from last year’s Moowsletter of how franking credits work.

What are Franking Credits?

Imagine later this year when you lodge your tax return, your accountant tells you the tax office owes you a tax refund because you’ve paid too much tax. But then in the same breath she says you won’t be getting the refund because the ATO has decided to keep it!

That’s what Bill Shorten’s proposed changes to franking credits look like. All superannuants, retirees and low-income earners who own dividend paying shares will be denied the tax refunds they are due.

And I’ll prove it to you with one simple line in just a moment.

But firstly, I want to address the three most common lies Mr Shorten has been using to mislead voters.

Lie Number 1 – it closes a loop hole

Mr Shorten claims that by removing franking credits it will close a ‘loophole’ that has been exploited by the rich. It’s not a loophole at all. Its Government legislation that was passed by both houses nearly twenty years ago.

The Truth About Lie #1

The implementation of tax credits by Peter Costello in 2000 was applauded by the Labor Party. In fact, Labor were so happy when it was introduced, they were gushing like teenagers because it was the epitome of socialism. Meaning, everyone would be treated fairly, most of all low-income earners. But don’t take my word for it, ask your accountant.

Lie Number 2 – franking credits steal from ‘schools and hospitals’.

This is rubbish. The ‘schools and hospitals’ pitch is an old, worn-out line that politicians use to pull at heartstrings and guilt anyone who opposes their ideas.

The Truth About Lie #2

If you’ve paid too much tax, you are rightfully entitled to a refund. It doesn’t mean you are taking money from schools and hospitals. That money is yours.

Franking credits are the same. They are only paid out when people have paid too much tax on dividend paying shares, just like personal income tax.

Lie Number 3 – franking credits favour the rich

This is perhaps the worst lie of all. It so deceitful. Franking credits do not favour the rich at all.

The Truth About Lie #3

Franking credits favour retirees and low-income earners the most.

It’s very simple. The less income someone earns the more franking (tax) credits they receive because of the excess income tax they have paid on share dividends…which is only fair.

If franking credits are removed, they will disadvantage superannuants, retirees, and low income earners the most. High income earners will not be affected. Again, just ask your accountant.

Let me show you why…

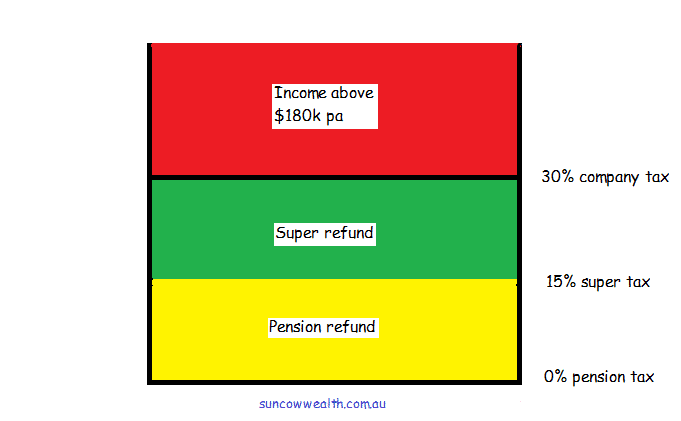

The easiest way to understand the proposed tax changes can be understood with ‘the line’. It works like this:

1. Company dividends are taxed at 30%. Therefore, 30% becomes ‘the line’. (see below)

2. This means, anyone with a marginal tax rate (MTR) greater than 30% sits above the line and anyone with a MTR less than 30% sits below the line. (Below the line is anyone who earns less than $180k pa including superannuants and retirees).

3. If you sit below the line, it means you’re entitled to a tax refund on company dividends because you’ve paid too much tax, just like your personal tax return. However…

4. Under Shorten’s proposed tax changes, he no longer wants to reimburse the group below ‘the line’ even though they’re entitled to a tax refund. In other words, he wants to keep the green and yellow sections normally refunded back to superannuants, retirees and low income earners, for the Government. Therefore…

5. Retirees will be the most disadvantaged group because they have a MTR of zero percent (0%) but will be taxed at 30% on share dividends. For some retirees, this will mean a drop in income between 25-33%.

Bill Shorten’s Referendum on Wages

Bill Shorten has called this next election a ‘referendum on wages’.

Really.

If he feels so strongly about wages and living standards, why is he short-changing low income earners and self-funded retirees on franking credits?

We (Suncow) have just finished last years tax returns for SMSF’s and if franking credits are removed, our client’s average income for retirees will drop by 22%! That’s right, twenty two percent.

And let’s be clear about this. We’re talking about a group of people who should be peacefully retired, not sitting bolt upright in bed worried about a drop in income and thinking of re-entering the workforce in their late sixties and seventies to replace what Shorten and Bowen have taken from them.

At the same time, Mr Shorten wants to introduce a minimum ‘living wage’.

The hypocrisy is breathtaking.

The minimum wage work won’t work for one of two reasons. Either;

I. Businesses will have to lay people off because they can’t afford to keep them, especially small businesses; or

II. Businesses will just pass the costs onto customers and force up the cost of living. Another hit for retirees, especially those denied any franking credits.

Incredibly, Bill Shorten has also promised to do something about gender inequality and closing the wage gap.

If that’s the case, consider this…

Widows Affected the Most

One of the largest cohorts to be affected by the removal of franking credits is widows.

Which begs the question, what happened to gender equality? And why haven’t we heard from Penny Wong, Tanya Plibersek, et.al? Or do we only play the gender card when it’s convenient, not when its important?

Mind you, the coalition are no better. They have more female members than any political party, yet we haven’t heard a peep from them either. So I can only assume their silence is also their support.

On this point alone, both sides of parliament ought to hang their collective heads in shame. It’s absolutely disgraceful.

Just another Mining Tax

The abolition of franking credits will be just another mining tax. It will yield nothing but ruin plenty, especially investor confidence.

This policy change will be a dud because investors will simply switch out of franked dividend paying shares and deny a Shorten govt the tax revenue it expects.

Instead, investors will put their money into property trusts, other managed funds and overseas investments.

A Sleeping Giant Awakes

When Bill Shorten first announced the proposed changes to franking credits, negative gearing and an increase in capital gains tax, the Labor Party was lapping Malcolm Turnbull in the polls.

Most of all, they knew Turnbull wouldn’t strike a blow and defend franking credits. And they were proven right.

The problem is, the Coalition have been spineless in defending franking credits ever since which is the only reason you are reading this. It should never have got this far. And the electorate is angry.

Both the Government and Opposition have severely underestimated how unhappy voters are. They have awoken a sleeping giant and now the giant is desperately looking for a friend.

And it pains me to say it but, the big winner out of all this could be the giants new friend, Clive Palmer.

The tables may turn again which means this war is far from over.

Warning: This Moowsletter may not be for you. If you get a little starry-eyed every time you glance at that gold band wrapped around your finger…look away now. I’m about to wipe the lust out of your peepers. (No hard feelings.) Here’s the unpolished truth about gold… If you bought $1 worth of gold 100 years …

Retirement should be a time to enjoy life, not stress over finances. A well-thought-out retirement plan ensures you can live comfortably, pursue your passions, and handle unexpected expenses without worry. The earlier you start planning, the smoother the journey will be. Let’s break it down into simple, actionable steps to help you create a retirement …

Continue reading “How to Plan for Retirement: Your Roadmap to Financial Freedom”

It’s Tuesday lunch, and all morning the markets have been drowning in a sea of red thanks to Trump’s tariffs. Investors are freaking out. But as my RM’s hit the pavement for my midday walk, I get this deep, unshakeable, hunch… “What if?” This is why my tummy turned… A month ago when Trump first …

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.